Brave New World

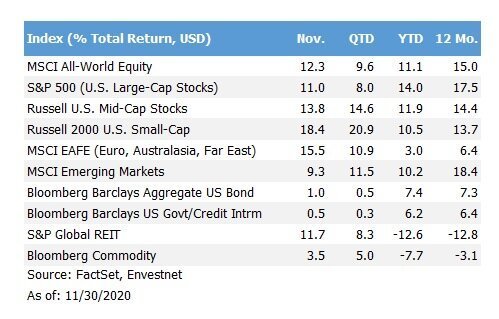

As a COVID-19 pandemic continued to surge, the stock market put in one of its best months on record. Investors are encouraged by positive news on the efficacy of several vaccines and looking ahead to a return to more normal economic activity. Global stocks gained 12.3%, the best month for the All-Country World Index since its creation in 1987. The bond market advanced a more modest 0.5-1.0%.

The excitement around vaccines overshadowed the much-anticipated presidential election. Fears of drawn-out legal battles or other disasters have given way to a somewhat orderly, if atypical, transition of power. It now looks as though the U.S. government will most likely be divided, with Democrats controlling the executive office and the House of Representatives, and Republicans maintaining the edge in the Senate. Historically, such divided a government has given investors confidence that neither political party will surprise the markets with sweeping new policies.

It may strike some as odd that the market reacted so positively as the pandemic intensified. But the idea that a highly effective vaccine would soon be available overshadowed the gloomy near-term outlook. As always, the value in stocks is derived from economic growth over many years, not the next quarter or two, so it is not surprising that vaccines may help inoculate investors’ economic concerns, as well as their health.

While the market’s overall performance is extraordinary, underneath the hood the rotation out of technology stocks into traditional sectors is well underway. Value stocks, which can be bought at more attractive prices, outpaced pricier higher-growth companies by 4.3% in November. The rotation also benefitted smaller U.S. firms and many international stocks, or basically everything other than the large technology companies that have been at the forefront of the market’s gains for the past several years. Apple, Amazon, Microsoft, Alphabet, and Facebook, the largest stocks by market value in the S&P 500, underperformed the broader market.

An effective vaccine is undoubtedly good news for the world and for the financial markets. Still, it will take time for economic activity to return to normal. The pandemic, stretched out over most of 2020, will likely leave some economic scars. Many businesses have shuttered, and some jobs may be permanently lost. Those wounds will take time to heal, but the economy will eventually recover as new businesses and jobs replace the old. Investors will need to evaluate the ability of companies to weather the potential, and yet undetermined, long-term impacts of COVID-19.

The markets continue to reward those who commit to a good long-term strategy, even when it seems the world, at times, is falling apart. Global stocks fell over 31% at the low point in March. Now, global stocks are up over 12% YTD, including dividends. The incredible volatility this year reminds us that successful investing doesn’t depend on timing the markets but on finding a strategy that you can stick with. Control over what the financial markets do in any given month or year is an illusion. It’s best to focus on how your money best fits your circumstances.

FOCUS ON PLANNING

The end of 2020 is fast approaching, and it is a good time to think about year-end planning. While your personal situation is unique, here are a few important items to keep in mind:

The CARES Act waived the requirement to take required distributions (RMDs) this year from traditional IRAs, inherited IRAs, and inherited Roth IRAs. For some, it may still make sense to make distributions from these accounts to take advantage of lower tax brackets that may otherwise go unused.

Consider potential Roth conversions. If 2020 was a low-income year, it may be a good time to convert some pre-tax IRA savings into a Roth at relatively low tax rates. With RMDs waived, there is an opportunity to convert what would have been an RMD to a Roth, shielding those funds from future taxation, possibly at higher rates.

Regular gifting can help reduce potential estate taxes. The IRS allows up to $15,000 to be given annually to any one recipient. Couples can effectively give $30,000. Gifts within these limits do not reduce your gift and estate tax exemption.

For some investors, funding an irrevocable trust to use part of the estate tax exemption could be an important planning tool. As a reminder, the lifetime gift/estate tax exclusion for 2020 is now $11.58 million, or potentially $23.16 million for a couple. The IRS has indicated that individuals who take advantage of the increased exclusion will not be adversely impacted (no “clawbacks”) if the exclusion is reduced or when the current law sunsets on January 1, 2026.

Review capital gains and investment income for the year. During the market decline in March and April, we sold many stocks that dropped in price and replaced them with similar stocks to maintain investment positions. Because of this tax-loss harvesting, we may be able to complete any needed year-end rebalancing of equity positions without significant increases in capital gains over 2019. Regardless, it may make sense to realize gains this year at what could turn out to be historically low tax rates.

Distribute trust income. Since higher tax brackets are reached more quickly for trusts, it often makes sense to distribute interest and dividends earned to beneficiaries who may be in lower tax brackets.

As always, it’s a good idea to consult your tax and estate planning advisors. We are reviewing client portfolios for year-end planning opportunities, but please let us know if you have any particular questions or concerns.

Best wishes for a peaceful and safe holiday season.

Contact us at 865-584-1850 or info@proffittgoodson.com

Please see disclosures